Polish people often complain about our healthcare system. Queues to see the specialists or have a surgical intervention take ages, when it comes to physical rehab one should sign up before the accident even happened and all-in-all the quality of service is also lacking on few parts. That’s why I wanted to demonstrate how it looks in the land of pisco and manjar.

Let’s start with the basics. In Chile every single working person (for now only people with full-time contract are obligated, however since 2018 independent workers will also participate) and pensioners (though according to the latest news this obligation won’t last much longer) have to pay at least 7% fee from their income.

The system itself can be divided into 2 parts: public (Fonasa) and private (Isapre). By default everyone is signed up for Fonasa. Even if previously they were using a family healthcare plan paid by their parents, first two months of working on your own means being covered by the state. After this time you can change your insurer. Apart from those two there is also the AUGE fund which takes care of all the high-mortality conditions (I will come back to this subject a little bit later).

QUICK REMARK: you cannot be insured by Fonasa and Isapre in the same time. AUGE functions completely apart.

How many people uses private insurance? According to the data from 2009[1] 75% of Chileans uses the public system. It’s quite interesting, because most of people I’ve talked to speaks very highly about private clinics (Isapre) and would like to be treated over there.

So why do people try to avoid public hospitals so much? Let’s let Pablo tell us his story:

Once upon a time we decided to go for a beer with a friend. It happened somehow that during drinking, the bottle cracked and cut his lips and inside of the mouth. Lots of blood. At that point we had a choice: drive 45 minutes to the clinic or walk to a nearby hospital. Since he was bleeding a lot, the option #2 won. We entered the ER and as usual we could see all the stabbed, people with ripped out fingers. We walked to the nurse who’s qualifying the new coming patients. Just as a reminder: friend had all his face smeared with blood. She looked at him and commented “ah, you’re alive. Go to the end of the line.”

So why only 15% chooses the private clinics?

Payment, payment, payment

Quoting Milton Friedman:

There is no such thing as free lunch.

Chile is a country which believes in free market and capitalism, where nothing is for free. That’s why free of charge public healthcare is available only for homeless or those who earn less than $210.001 Chilean pesos (320 USD / 290 EUR) gross each month. If the person earns between $210.0001 and $306.000 CLP (465 USD / 425 EUR) then has to participate with 10% of the cost. However if the income is greater than $306.000 CLP then the participation grows up to 20%[2].

So remembering Pablo’s story and other of that sort, a question arises. Why people don’t choose Isapre more often?

The question is if they can afford it.

Let’s take a generic Juanito Perez who earns that $306.000 CLP, but he doesn’t like the public healthcare system which grants him 80% of discount for any procedure (without any limits). Well in such case he still would have to pay some extra cash, because the 7% of his income doesn’t cover the minimal private insurance which costs around $27.500 CLP (42 USD / 38 EUR). But let’s check what does he get in return.

- Medical consult (ordinary doctor’s visit) with a discount of 80%. However the Isapre gives a top limit which it covers for each visit – $10.000 CLP (15 USD / 14 EUR). If you have more – the insurer won’t pay. When I had to go to a dermatologist (without the insurance), this wonderful experience cost me 40-53 USD / 36-49 EUR. You can count the difference

- Hospital treatment with a discount of 30% up to 90%. How much the Isapre covers depends on which clinic our Juanito chooses. The better the spot, the bigger the price. It’s not only because that the better clinic simply charges more for the same procedure, but also that the bonus changes depending on the clinic’s group type. Of course the surgery itself, doctors’ salary, meds and hospitalization are accounted separately (different discounts might apply). But let’s say that the procedure costs 40.000 USD / 36.400 EUR. The best case scenario (the worst clinic) our little hero would have to pay extra 4.000 USD / 3640 EUR. If he would like to have slightly better healthcare his participation goes from 8.000 USD / 7280 EUR up to 26.600 USD / 24.270 EUR.

And just to remind you: our little Juanito earns 465 USD / 425 EUR gross each month.

Of course these examples don’t cover everything and don’t demonstrate the whole offer. Not to mention… the clinics don’t have the same prices. But if you can see that one group has 25% coverage, while another – 90%, you can imagine what the differences might be.

Sex, age and other discriminations

Let me tell you a story.

With Mr. Beard we signed up for Isapre more less the same time. I’d also like to add that we had the estimate of our fees more less on the same level. So what’s the difference between the two of us? Age (technically I’m in the younger and cheaper group) and sex. The final result is the fact that Mr. B. has 90% of discount for the clinics, while my little person – 70%.

“But why?”, sprouted soon in my little brain. I started to look for more information concerning this topic, since most of the insurers shares the tools to calculate your plan depending on your income, age and sex.

And here’s where it gets interesting. Changing only my gender (date of birth, preferred hospitals, etc. stayed the same) I got two completely different plans. If I were a man, I got the option of 100% discount in preferred clinic without any limit of costs. However while being a woman – the discount goes down to 80% and a limit shows up.

But… but… I forgot to mention one important detail. All those plans don’t cover pregnant women. So what would happen if I would be expecting a little alien? There are 3 options:

- I could pay more for a plan that takes care of pregnancy, labour and junior’s med care,

- I stay with what I have, but then my discounts plunge down from 70% to 30%,

- I ditch Isapre and switch to Fonasa.

In this very moment the only thing I could say is that as a woman, I’m completely screwed. So I decided to change my approach and check how much would I have to pay to get the same plan as a guy.

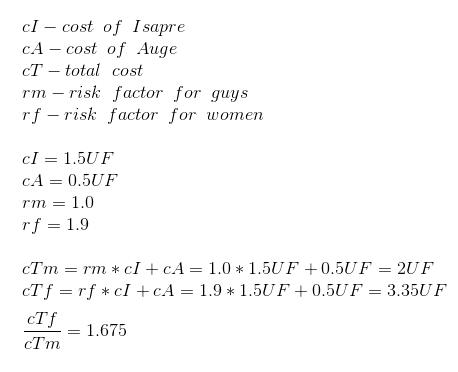

Isapre in its files has “risk factors” when it comes to age and sex. So let’s do a quick estimate (simplified, I assume the income of 1650 USD / 1500 EUR):

calculations based on ASPEN 15013 Colmena Golden Cross

Ergo as a woman I have to pay extra 68% to have the same insurance as a man in the same age.

And since we mention age. Let’s check how the differences look like when the years fly by.

| age | man | woman | ||||

| CLP | USD | EUR | CLP | USD | EUR | |

| 20-25 | 38 312,58 | 58,31 | 53,06 | 47 733,70 | 72,65 | 66,10 |

| 25-30 | 42 081,03 | 64,05 | 58,27 | 66 575,95 | 101,33 | 92,20 |

| 30-35 | 47 733,70 | 72,65 | 66,10 | 81 649,75 | 124,27 | 113,07 |

| 35-40 | 53 386,38 | 81,25 | 73,93 | 81 649,75 | 124,27 | 113,07 |

| 40-45 | 62 807,50 | 95,59 | 86,98 | 81 649,75 | 124,27 | 113,07 |

| 45-50 | 66 575,95 | 101,33 | 92,20 | 92 955,10 | 141,48 | 128,73 |

| 50-55 | 81 649,75 | 124,27 | 113,07 | 100 492,00 | 152,95 | 139,16 |

| 55-60 | 104 260,45 | 158,68 | 144,38 | 111 797,35 | 170,16 | 154,82 |

| 60 | 160 787,20 | 244,72 | 222,66 | 157 018,75 | 238,98 | 217,44 |

calculations based on ASPEN 15013 Colmena Golden Cross

After analysing all this date I could only curse. Come on… it’s the 21st century, such things shouldn’t happen in the first place. And you know what? It turns out that in 2010 Chilean Constitutional Tribunal declared that such discriminations based on age and gender when it comes to health insurance is illegal[3]. So why the heck 5 years later this problem is still alive and breathing? Well… The Tribunal left this with the president(s) to fix, while they said that Ispare should fix it on their own. Therefore the status quo still exists, because who would want to kill the goose that laid the golden eggs.

However there’s a light in the tunnel. This discrimination (gender or age) got banned in the public healthcare system. The same thing happened with pregnancies. In 2014 the state finally declared that pregnancy is not an illness and they would cover 100% of the expenses.

AUGE

Last but not least… What happens if you’re terminally ill. When it comes to that AUGE, being short for Acceso Universal con Garantías Explícitas, is might be your best friend. Why only “might”? In this very moment there are only 80 conditions on AUGE’s list, so it might happen that the illness is only covered by Isapre or Fonasa.

AUGE was created so people could get the best care as soon as possible and close to their homes. However even here we go back to the problem of partial payment which can go up to 20%, but in the same time the total doesn’t exceed one month of income for the family in a year.

And here I would like to show you an example. I had a chance to chat with a person who suffers from multiple sclerosis. To have the illness under control they have to take meds which 1600 USD / 1450 EUR[4]. Every month. Thanks to AUGE this cost goes down to 270 USD / 240 EUR which still has to be covered by the patient.

I left the most interesting titbit for the last: SM was put on the list in 2010. Before that people had to take care on their own.

Summing up

What can I suggest to people who want to visit/live in Chile? Don’t get sick. And additionally pack yourself into Zorb ball, because someone can still hit you with a car.

Mr. B. suggests also another solution – to earn millions.

And yes, I know that often the state insurances (in Europe, Poland especially) are terrible. As much as I vote “yes” for partial payment, be it for getting extra cash flowing in the system or some psychological trick to make the lines shrink, I also wanted to show you, what happens if you leave the “free market” on its own. Because “it will regulate itself.”

Bullshit. Wishful thinking.

Apart from the fact, that the weakest always get hit the most… Such discrimination when it comes to such basic and important thing as healthcare, is simply and freaking unfair.

—

[1] https://en.wikipedia.org/wiki/Healthcare_in_Chile#Beneficiaries

[2] http://www.supersalud.gob.cl/consultas/570/w3-propertyvalue-4008.html

[3] http://www.cooperativa.cl/noticias/pais/salud/isapre/tc-limito-uso-de-tablas-de-riesgo-de-isapres/2010-07-27/154453.html

[4] Interesting fact: before being put on the list, the price of these meds was 1060 USD / 970 EUR. As soon as AUGE started to pay the bills, the price went up.